We came upon an unpleasant surprise when venturing to use alternative_payee on invoices.

For reference, the following issued was filed and closed without resolution.

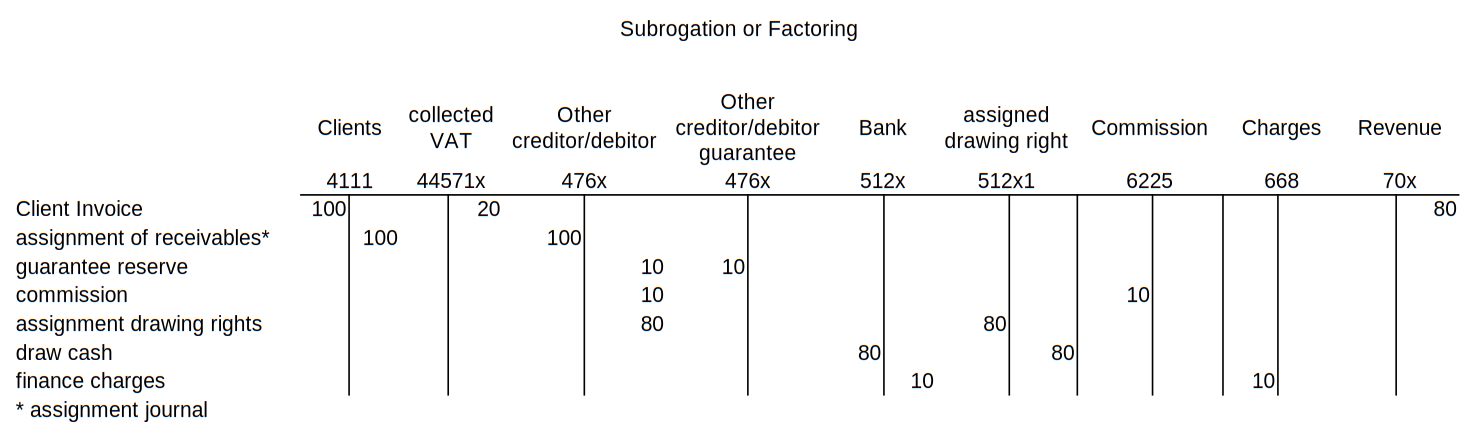

The use case is traditional Factoring

Indicating the alternative_payee party is, in this use case, a contractual obligation (for both suppliers and by the company for the clients ‘subrogated’). In fact,

In my opinion and experience, for corporate and, importantly, fiscal reasons, the invoice and related primary invoice moves to the GL are with the original supplier/client (‘in’: party == supplier, ‘out’: party == client) as usual.

But the problem encountered is that instead of creating the normal invoice move, the alternative payee is indicated in the invoice move, which poses a number of problems.

On the invoice, the most important element is the bank account, plus some legal text concerning the subrogation.

There can be numerous moves made following the accounting life of these invoices, in particular for those on a cash-basis (where payment date by the client is the event determining whether VAT is due).

I came across this site (in French) that gives some examples of the various forms available from one such Factor, including accounting move summaries

Perhaps there needs to be others mechanisms put in place… observations?

Cheers