At least in Spain (and I guess in another countries too), the financial entity charges you a quote by the leasing contract through an invoice with taxes.

The problem here is that one of the invoice lines (“product”) account is not an expense or revenue account, so I cannot select it then I do not know how I should book that invoice.

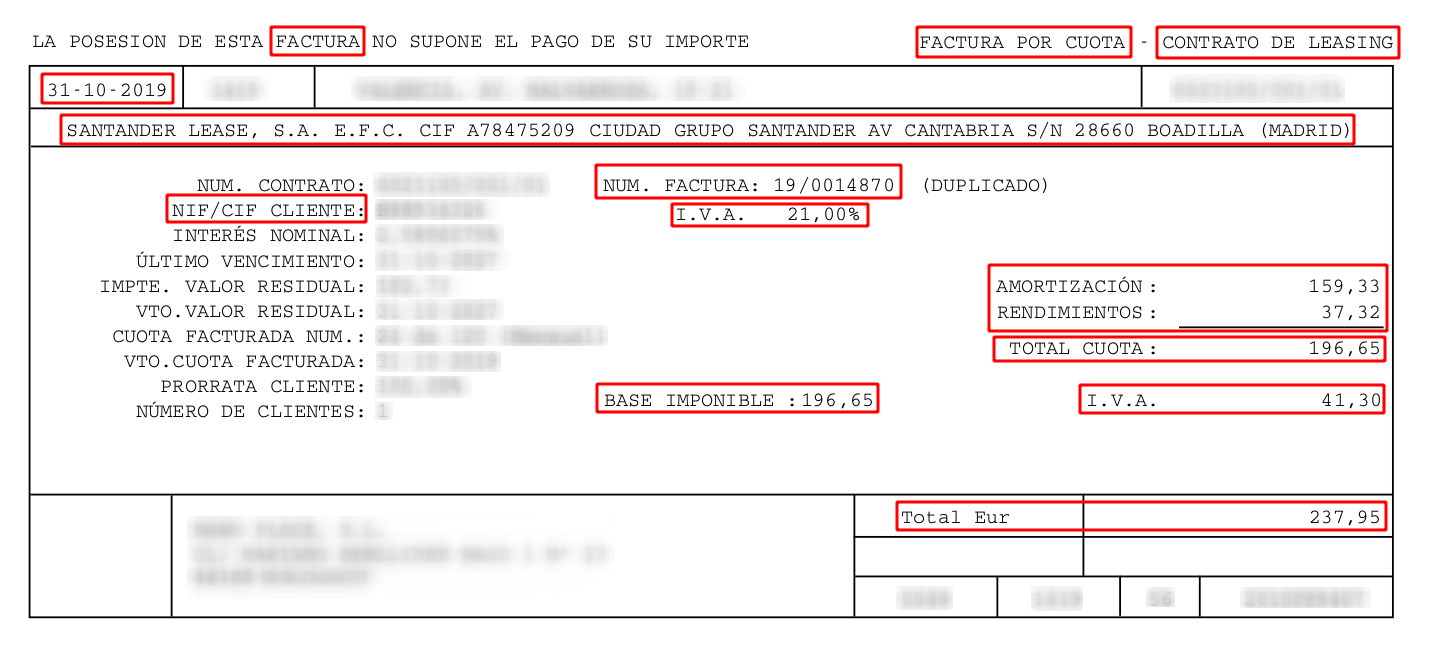

Factura: Invoice

Factura por cuota: Invoice by quote

Contrato de leasing: Leasing contract

Santander Lease…: party (financial entity)

NIF/CIF cliente: Customer tax identifier

Num. Factura: Invoice number

I.V.A.: Tax percentage applicable

Amortización: Invoice line (to book to an account type distinct from revenue or expense - this is the problem)

Rendimientos: Invoice line (to book to an expense account)

Total cuota: Total invoice amount excluding taxes

Base imponible: The same as above

I.V.A.: Total taxes amount

Total Eur: Total invoice amount including taxes

OK so the amortization is directly booked from the invoice.

So for me, you need to account_asset module and have the type “Acreedores por arrendamiento financiero” set as fixed asset. But I would not create a product for this case because you are not managing a depreciation (or only at the end of the leasing).

I do not see this is possilbe as fixed assets are only for assets but this account is not an asset but a creditor account. Normally this account is used as counterpart of the asset in order to record the liabilty that you have to pay the total amount of the leasing to the leaser.

I’m wondering if it won’t be better to include a check (probably on account_asset module) to indicate that the account is fixed asset liability and include them on the invoice. So we allow to include also this kind of accounts on invoices.

In this case you have the amortization of the leasing not the amoritzation of the asset which may be diferent. The deprecation of the asset normally lasts longer than the duration of the leasing. Let me put an example.

You buy an asset valued at 100.000€ which has a deprecation duration of 10 years. To buy them you use a leasing of 5 years for a fixed monthly amount. The invoice which we are talking about is the invoice for the payment of the leasing, which include the credit amortization (account 524), the interests (account 662) and the taxes (account 472).

I’m not an accountant so I try to look for one to ask this question but, in essence, when you are leasing an active, this active owns to financial entity until you satisfy the last payment, so you don’t have to do any amortization. I think…

The account which @josesalvador wants to introduce as line is not asset nor amortization/deprecation. It is the payment of leasing credit to the leaser.

The asset and amortization/deprecation details are not included on the invoice. This is something that should be managed like assets that are bought without leasing.

So it is a little bit like the deposit account. But I do not know how it should be named, I think liability is too generic because I do not think all of them can be added on an invoice.

In Spain MicroPYMES are allowed to book leasings directly as expense.

Otherwise you have to book two facts:

The fact that you bought an asset. This should use the standard asset module.

The fact that you have the liability to pay the amount for the asset. This is like a credit with a bank.

Once the leasing is fully paid there is two possilibities:

If you keep the asset you have nothing to book as it will continue to depreciate normally.

If you do not keep it you have to remove it from your assets, matching the depreciating amount with the amount that you have paid for the leasing. This can be done in advance by updating the asset residual amount and end date when the company knows that is not going to keep the asset.

I agree that liablity is too generic. Probably something about leasing as I do not see any other use case.

When you have a credit with the bank they do not issue any invoice and you register they payments when importing the statement.